When you’re facing a large tax bill, it can feel like there’s no way out. That’s where an Offer in Compromise may come in. It’s a program through the IRS that allows some taxpayers to settle their debt for less than the full amount owed, offering a path toward real financial relief.

Many people don’t realize this option exists. The constant letters and penalties can make it seem like the IRS will never negotiate or show leniency, but that’s not the case. The IRS understands that some taxpayers simply cannot afford to pay everything they owe and provides several programs designed to help.

If your tax debt feels unmanageable, learning how the Offer in Compromise works and whether you might qualify could be the first step toward regaining control and moving forward.

What Is an Offer in Compromise?

An Offer in Compromise is one of the IRS’s main tax relief programs, created to help taxpayers who owe more than they can reasonably pay. Rather than demanding the full balance, the IRS may agree to accept a smaller amount that reflects your true financial situation.

The program is built on the idea of fairness. The IRS reviews your income, expenses, assets, and ability to pay, then determines whether collecting the full amount would cause financial hardship. If so, they may approve a settlement that resolves your debt for less than you owe.

However, an Offer in Compromise is not available to everyone. The IRS accepts only a small percentage of applications each year, focusing on cases where full payment is unlikely. Understanding the specific qualifications is key before deciding whether to apply.

Who Qualifies for an Offer in Compromise?

Not every taxpayer with debt will qualify for an Offer in Compromise. The IRS only approves offers when it believes the amount being offered is the most it can reasonably expect to collect within a certain period of time. In other words, it’s designed for people who truly cannot afford to pay their full balance.

To be considered, you must be current on all required tax filings and payments, and you cannot be in an open bankruptcy proceeding. The IRS also reviews your entire financial picture before making a decision. This includes your income, monthly expenses, assets such as property or vehicles, and your future earning potential.

The goal is to determine whether paying the full debt would cause financial hardship or prevent you from meeting basic living expenses.

If you believe you may qualify, understanding how the Offer in Compromise process works can help you prepare and avoid mistakes that could delay or derail your application.

How Does the Offer In Compromise Process Work?

The Offer in Compromise process may seem complicated at first, but it can be broken down into a few clear steps. Each stage is important, and accuracy matters. Small mistakes or missing information can cause significant delays or lead to a rejection.

1. Financial Review

Before you apply, the IRS requires a full review of your financial situation. This is done using Form 433-A (for individuals) or Form 433-B (for businesses). These forms detail your income, expenses, assets, and debts. The IRS uses this information to calculate your “reasonable collection potential,” or how much it believes you can realistically pay.

2. Submitting an Offer

Once your financial information is complete, you’ll submit Form 656, which officially presents your offer to the IRS. You must also include a non-refundable application fee and an initial payment based on your chosen payment option. Offers can be paid as a lump sum (typically 20% upfront) or through monthly installments spread over time.

3. IRS Review Period

After your submission, the IRS will carefully review your application, a process that can take six to twelve months or longer. During this period, the IRS may request additional documents or clarification about your financial details. Responding promptly and accurately is crucial to keeping your case moving forward.

4. Decision and Compliance

If your offer is accepted, you must follow the agreed payment schedule and remain compliant with all tax filings for the next five years. Failure to file or pay on time during that period can cause the IRS to revoke your agreement, reinstating the original balance. If your offer is denied, you can appeal the decision within 30 days.

Because the process involves detailed financial documentation and strict compliance rules, having professional guidance can make a significant difference. An experienced tax professional can help ensure your forms are complete, your offer is realistic, and your submission meets IRS expectations.

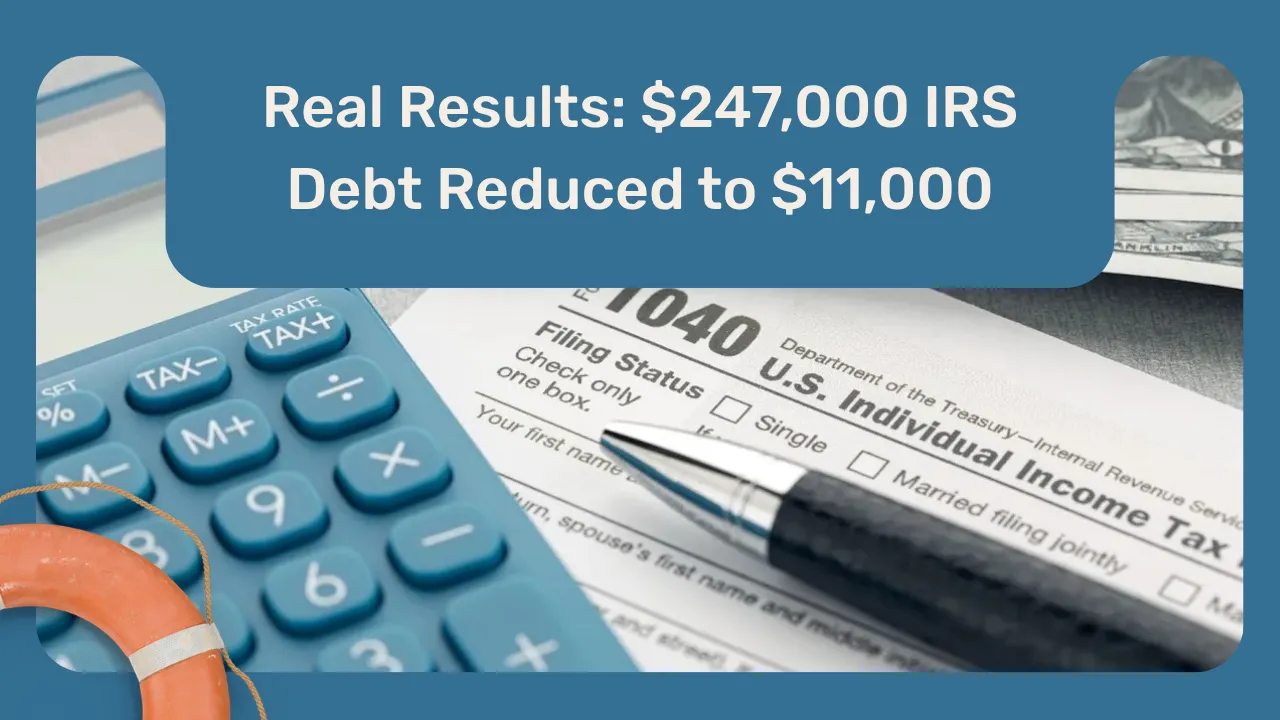

Case Study: Turning a $260,000 Tax Bill into Relief

Real stories show just how impactful the right tax resolution strategy can be. One client in Dallas owed the IRS more than $260,000 and felt completely overwhelmed by the weight of that debt. His only goal was to be able to “sleep at night” without the constant stress.

After a careful review of his financial situation and communication with the IRS, Tax Lifeline was able to negotiate a resolution that reduced his balance to just $11,000 — a total savings of more than $247,000.

While every case is different and results vary, this example shows that meaningful relief is possible when you take the right steps and work with professionals who understand the system.

Common Mistakes That Cause Offers to Be Rejected

Even when taxpayers meet the basic qualifications, even the smallest errors can lead the IRS to reject an Offer in Compromise. The most common issue that we see is submitting an application before all required tax returns have been filed or if there are unpaid current-year balances. The IRS will not consider an offer if you are not fully compliant.

Another frequent mistake is proposing an unrealistic offer amount. The IRS bases its decision on your financial data, so lowball offers that do not reflect your true ability to pay are typically denied.

The last critical mistake to avoid is failing to respond in a timely manner to the IRS when additional information is requested. It is very common for the IRS to request additional documentation once an application is received. Failing to respond to these requests automatically disqualifies the application.

Many of these rejections could be avoided by carefully reviewing eligibility, staying current on filings, and submitting complete, accurate documentation from the start.

How Tax Lifeline Can Help

Navigating the Offer in Compromise process takes time, patience, and precision. Every form, figure, and piece of documentation matters, and even a small error can cause unnecessary delays or rejections. That’s where having the right guidance makes all the difference.

At Tax Lifeline, we help taxpayers understand whether an Offer in Compromise is truly the right fit for their situation. Our team reviews your financial information, ensures your filings are up to date, and prepares a complete, accurate application that aligns with IRS requirements. We also communicate directly with the IRS on your behalf and explore every available resolution option, including installment agreements or currently not collectible status if those better suit your needs.

If you’re struggling with tax debt, don’t face it alone. Reach out to the team at Tax Lifeline to find the most effective path to relief and start fresh with confidence.

Ready to be pulled to safety?

Grab the lifeline and let’s get you the freedom from tax debt you deserve!

Schedule A Consultation